We're highly recommended by our clients

5.0 stars from 16 google reviews

Is this you...

A Home Buyer

Information and tips for home buyers planning on purchasing their first (or next) home in the near future…

A New Investor

Advice and support for new investors looking to start generating wealth through property investment…

An Established Investor

Resources and strategies for established investors with large or complex portfolios…

Access free loan structuring advice to avoid future complexity and broaden your choice of lenders

Ryan took care of everything for us and made the whole process very easy. He was very diligent in relation to communication, ensuring we were kept up to date. We appreciate that he went the extra mile in making sure our needs were addressed and we meet key deadlines. – Cam Bell

Establish your borrowing capacity upfront & learn if / or where your lending limitations exist

The team at Next Home Loans have done a fantastic job helping me with my property goals. The professionalism and engaging manner, particularly from Ryan, has made dealing with the financial aspects of our property ambitions easy and enjoyable. – Pete Bain

Understand your borrowing options & the strategies available to you for opening up lending channels

Gain cashflow certainty with upfront repayment comparisons & itemised purchase cost breakdowns

Borrow Better with industry leading support

We'll save you time

We help you find a lender quicker without having to visit banks or waste time filling in loan applications from scratch – wherever possible, we do the work for you.

We'll save you effort

We’re familiar with the information each lender requires and how it should be presented. We do everything we can to ensure that the application process is as smooth as possible.

We'll save you frustration

We help ensure your loan application meets the lenders requirements before submitting, so you’re much less likely to experience the frustration of being knocked back by a lender.

Getting started with the Right loan is easy...

and we’ll ensure you are informed and empowered every step of the way.

Schedule a call

Simply fill in and submit the appointment booking form and one of our friendly staff will be in contact with you.Let us know about you

We’ll get an understanding of what you’re looking to achieve, so we can determine the best path forward.Present your options

We’ll provide you with estimated repayments, borrowing capacity, deposit requirements, & loan recommendations.

What to expect once you’ve scheduled a call…

We understand you’re looking for the right mortgage broker to work with – following up from your enquiry, one of our mortgage brokers will call, at the time you designated, to introduce themselves and vice versa.

We’ll take the time you need to answer any questions you may have, we’ll enquire about your situation, the challenges you face, and the borrowing goals you have.

Depending on how time-critical your lending needs are, we can immediately discuss your purchasing requirements and next steps. Where possible we can triage any issues that could affect your ability to secure a loan and help you to identify strategies for mitigating those issues.

We’ll never talk down to you or make you feel like a ‘fish out of water’. You’ll be in good hands and together we’ll discuss how we can make your borrowing goals, a reality.

This certainly isn’t a high-pressure sales call. It’s a chance to see if we’ll work well together.

After your initial phone conversation, and if you are happy to move forward, your broker will request some supporting documents and begin preparing your loan strategy proposal.

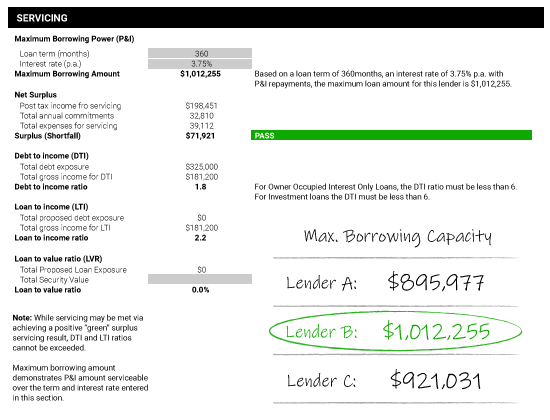

This is the preliminary assessment process and is a very detailed stage where we identify any possible problems from a lending point of view. We also calculate your borrowing capacity (or how much you can borrow) and assess which lenders can assist and compare the most suitable loans at the lowest interest rates.

In preparing your proposal we will lay out the framework for your lending structure, detail deposit requirements, purchasing costs, what banks will lend to you based on policy, what rates and features may be most appropriate, and how to structure your loan(s) to be most flexible and cost effective.

It may surprise you to learn our preliminary assessment process is the same process that we use when you are applying for a full home loan – We go through the banks’ actual credit criteria to make sure you are eligible and will qualify for a loan and our internal credit team performs an extremely thorough analysis of your goals and finances.

We view this stage as the most important step in the process, as it ensures we are short-listing the right lenders and formulating a thoroughly tailored loan strategy proposal that is centred around your goal(s) and in your best interest.

Your Loan Strategy Proposal document is designed to walk you through an analysis of your situation, provide an explanation of your loan options, recommendations and highlight the analysis that was used to support your recommendations.

Our loan strategy proposal is made up of 7 key areas with the single goal of securing you the best loan possible.

1. Goals & Objectives

It is important we accurately capture your lending requirements; we view this as a critical component to providing you with a great lending solution.

Your lending goals act as a foundation from which your loan application is created. What we mean by this, is it guides our team to compile your application, supporting documentation and provide commentary in a way that highlights the strengths of your application and presents it in a particular way that suits the lender who will assess your loan. In essence, maximising your chances of approval.

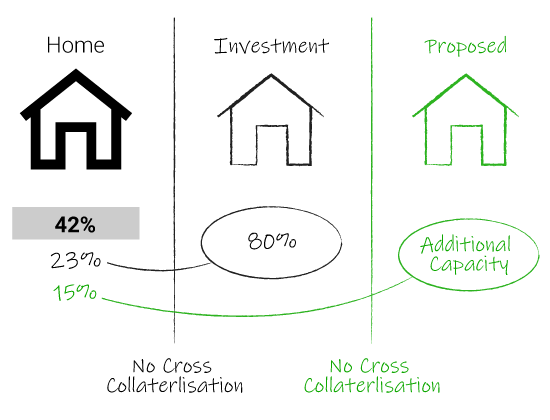

2. Funding Position(s)

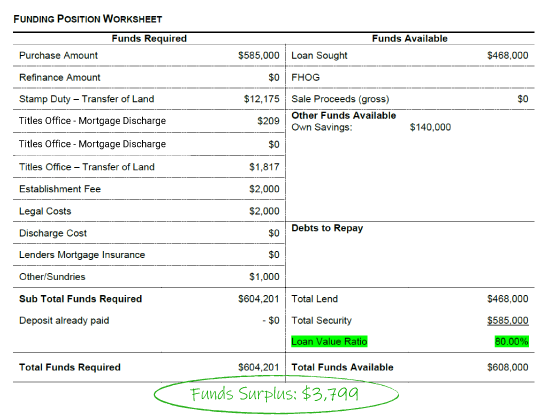

A very common question we get asked by our clients is, how much money will I need to set aside to complete my purchase? This is where your funding position comes in to play.

Your Funding Position table outlines the funds required to execute your strategy and underpins the calculations we completed to confirm affordability. The funding position details your purchase amount (if available), purchase costs (title registration and transfer, loan establishment fees, conveyancing costs, building & pest inspection costs, discharge costs and outgoings), LMI amounts (if applicable), current funds available (available savings, gifts, guarantors), loan sought, and provides a total fund balance required to complete your purchase(s).

3. Lender Policy Matrix

Unlike dealing with a bank, we will consider many loan products from a multitude of lenders. During our extensive pre-assessment stage, we will consider lenders that you may or may not qualify for a loan with, depending on the lenders individual policies. The pre-assessment stage is designed to exclude the lenders you won’t qualify with and shortlist the lenders you will. The information provided in your lender policy matrix highlights the outcomes of these investigations.

Why is this important? You may not be aware, Australian banks and lenders mortgage insurers have specific lending criteria that they use to assess home loan applications. If your situation falls outside of their guidelines, your application is likely to be declined.

The good news for borrowers is lender policy can vary widely between lenders – where one lender has said no, another lender may be happy to write your loan. The goal of an experienced broker is to assess lender policy prior to shortlisting and recommending you loan products.

When it comes to a successful home loan application, there are several factors a lender may take into consideration, including your income (think PAYG, bonuses, rental income, gearing add-backs), savings, job stability, age, security (both current property assets and proposed purchases), borrowing intentions and the lenders own risk appetite. Then there are lenders that will auto-decline applications and others that will bend their criteria and consider your application based on its merits.

What is important here is you receive a complete picture of your lending options. If you are only discussing your lending requirements with a single lender, that may not be the case.

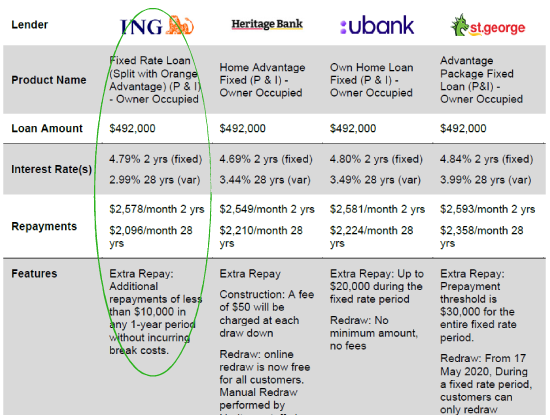

4. Comparison Report

As part of our pre-assessment process and in line with your lending goals, we eliminate lenders that don’t pass the policy filter and display a shortlist of lenders in your Comparison Report that you are eligible for, and will qualify to apply for, a loan with.

Your comparison report will show the various eligible lenders; current interest rates; monthly repayments; features; associated monthly fees; and discharge costs. Generally, your loan offerings will be ordered by total loan costs which is often a more accurate representation of the lifetime value of a loan, than interest rates alone as it factors in lender’s fees.

A comparison report is one of the unique benefits of utilising a mortgage broker to source your loan rather than dealing with a lender directly.

5. Highlighted Solution

With your comparison report proving you with a shortlist of eligible lenders, it is your turn to decide on the right loan product for you.

While the decision of which lender you would like to proceed with is ultimately yours, we will make a recommendation and support this recommendation with reasons why, based on the merits of the loan product and alignment to your lending objectives.

5a. Lending structure diagram – In addition to our recommendation, we include a diagram of your proposed lending to help you visualise your loan structure. This is the simplest way we’ve found to illustrate how your loan facilities will come together after settlement.

6. Supporting Information

For many of our clients, different loan features can sit high on their list of lending requirements. In addition to highlighting eligible lenders, we provide additional information and education related to the features noted or included within your proposed lending options.

Examples of Supporting Information can include sections on:

- Offset Accounts or impact of existing offset balances

- Impact of extra repayments

- Tax deductibility

- Construction loan process

- First home buyer schemes

- Pre-approval process

- Etc.

7. Next steps

With your loan strategy proposal complete, you should have a clearly articulated lending goal(s), a comparison of shortlisted loan options you would be eligible to apply for, a lending recommendation that has been supported by relevant reasons, and been provided with a clear understanding of the proposed loans features and inclusions.

What comes next is up to you…

Know that your mortgage broker will be there to guide you in your choices, and work as a conduit between you and the banks to find you the best loan possible and manage the home loan process all the way from pre-approval to settlement.

After your loan strategy proposal, there are three likely scenarios:

1. Getting You Ready to Buy

If we find any major issues that will affect your eligibility for a home loan that can’t be fixed in the short term – or you’re just not quite ready to buy – we will work with you over the coming months to get you to the point where you’re ready.

2. Pre-approval or Eligibility Letter

If there are no issues with your loan eligibility and you are planning on buying your home within the next three months, we will get our team to prepare a pre-approval or an eligibility letter you can make an offer or head to the auction with clarity and confidence.

3. Applying for Your Loan

If you’re red hot and rearing to go, or you’ve already put pen to paper on a contract of sale, we will proceed directly to lodging and preparing your home loan application.

We understand that everyone’s situation is unique, and your situation might not fit neatly into one of these scenarios. Rest assured that if this is the case, we will create a unique plan for you based on your goals and what you need.

Once you have chosen the most suitable loan for you, we’ll then prepare to submit your application to the lender.

We will ask you to provide any final documents and to sign the lender’s privacy form.

While we wait for these documents, we will prepare your application and upload it into the lender’s system or application portal.

We highlight the strengths of your application and present it so it suits the way that the particular lender will assess the loan.

Once we have everything we need, we click submit on the lender’s system and email your supporting documents to the lender.